All code for the project is available on Github: https://github.com/OpenSourceAP/CrossSection/

- Check out the code to understand how each signal is constructed

- If you find mistakes, please let us know by opening an issue

- If you want to provide code to construct additional signals, open a pull request to let us integrate it in the code base

In addition, we provide demo code to illustrate a few simple things one can do with the datasets that we provide: https://github.com/OpenSourceAP/CrossSectionDemos

- Each file is an independent script that automatically downloads data from the internet. You just need the googledrive R package and a Google Drive account.

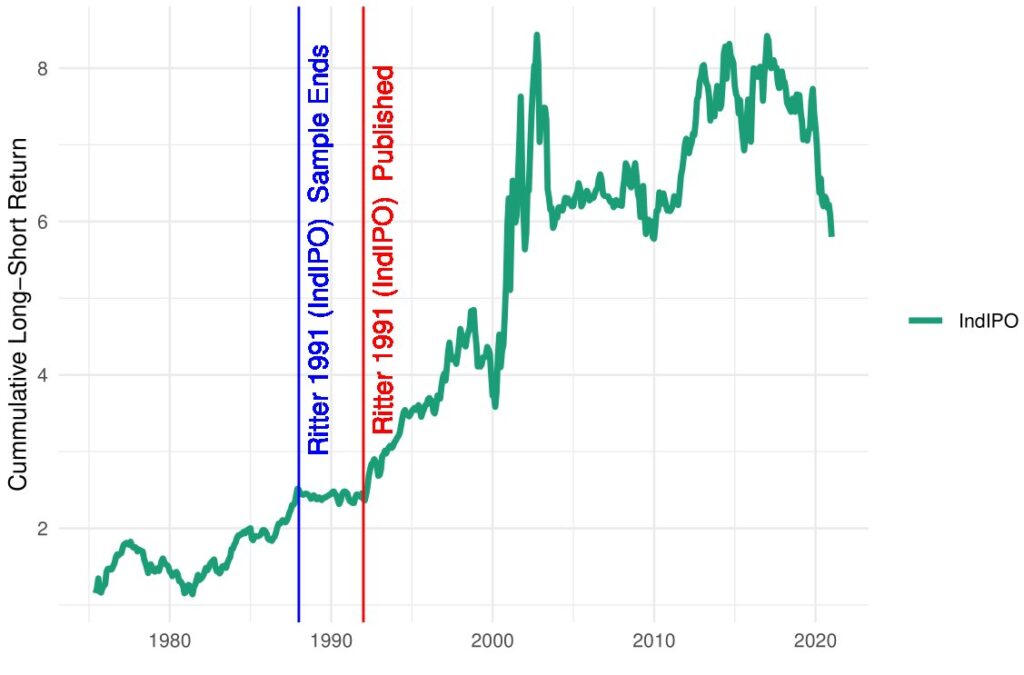

- For instance, the plot_anomaly.R lets you plot an anomaly’s cumulative return together with sample end and publication dates:

Code releases

- Currrent release (v2.0.0): Major Python signals translation update, annual improvements

- Previous release (v1.4.1): AnnouncementReturn lookahead bias patch

- Previous release (v1.4.0): Annual improvements

- Previous release (v1.3.0): New predictors, annual improvements

- Previous release (v1.2.0): New predictors, Fama-French style 2×3 portfolios

- Previous release (v1.1.0): Daily returns, more monthly implementations, completeness checks

- Previous release (v1.0.0): Major modularization update

- Older beta releases